Sie haben auf eine Website von Atradius zugegriffen. Indem Sie beliebige Funktionen dieser Website durch Anklicken nutzen, erklären Sie sich ausdrücklich und automatisch mit der Nutzung von Cookies zur Speicherung Ihrer Daten einverstanden, einschließlich des ersten Cookies, das beim Öffnen dieser Website gesetzt wird. Weitere Informationen zur Nutzung von Cookies und dazu, wie sie deaktiviert werden können, finden Sie auf der Seite mit Informationen zu Cookies.

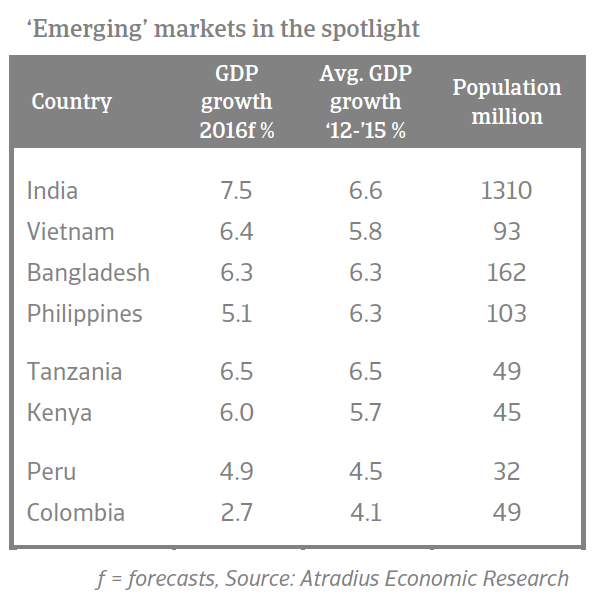

Atradius picks the top 8 markets for business opportunities in 2016. These emerging markets have been showing strong performances over the past three years and are expected to improve further in 2016.

Erhalten Sie Daten zum weltweiten B2B-Inkasso mit Publikationen von Atradius Collections wie dem International Debt Collections Handbook und der Global Collections Review.

There are positive signs for the Turkish chemicals industry. In 2015, the chemicals sector is expected to grow driven by increasing demand and the positive effects of the lower oil prices.

In Q1 2015, the Dutch chemicals sector saw an increase in production and exports. Additionally, it is expected that Dutch chemicals businesses ́ investments will increase in 2015.

In 2015 Italian chemicals production is forecast to grow 1.4 %, due to increasing exports (up 3.2 %) and the first signs of improving domestic demand (up 1.3 %) after four years of contraction.

The chemicals sector is benefiting from the on-going US economic growth. US chemicals production growth is expected to increase 3.7 % in 2015 and 3.9 % in 2016 (after growing 2 % in 2014).

German chemicals/pharmaceuticals businesses have a strong market position, and many are highly specialised. The industry has a well-deserved reputation for innovation and a competitive edge.

The chemicals sector ́s export share (mainly in Europe) amounts to more than two thirds of overall sales. French businesses are in strong competition with international players, especially the US.

The UAE’s ICT market is currently characterised by high competition, single-digit margins, low entry barriers and stagnating growth in sub-segments like PCs and desktops.

The German ICT sector generally has good growth prospects, but low margins, sharp price erosion and steep competition lead to an on-going trend of consolidation.