Sie haben auf eine Website von Atradius zugegriffen. Indem Sie beliebige Funktionen dieser Website durch Anklicken nutzen, erklären Sie sich ausdrücklich und automatisch mit der Nutzung von Cookies zur Speicherung Ihrer Daten einverstanden, einschließlich des ersten Cookies, das beim Öffnen dieser Website gesetzt wird. Weitere Informationen zur Nutzung von Cookies und dazu, wie sie deaktiviert werden können, finden Sie auf der Seite mit Informationen zu Cookies.

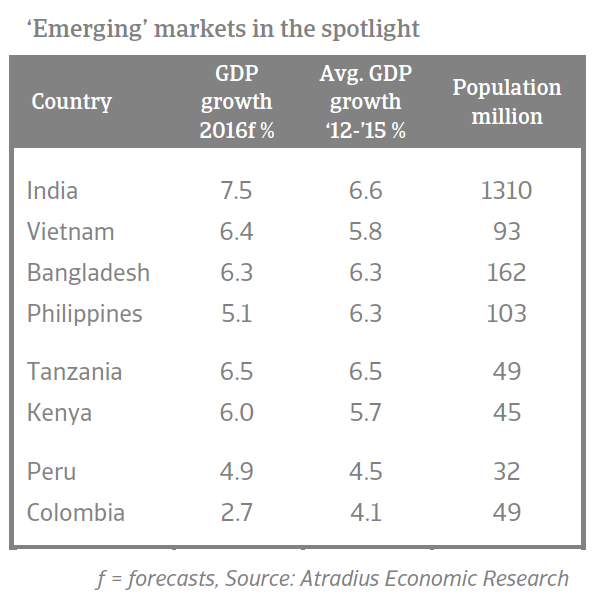

Atradius picks the top 8 markets for business opportunities in 2016. These emerging markets have been showing strong performances over the past three years and are expected to improve further in 2016.

Erhalten Sie Daten zum weltweiten B2B-Inkasso mit Publikationen von Atradius Collections wie dem International Debt Collections Handbook und der Global Collections Review.

Natural gas prices have fallen significantly in Asia and Europe on the back of the sliding oil price. As more LNG comes on the market regional prices are set to remain low.

Atradius survey shows an uptick in late payment of B2B invoices in China, which can have a knock-on effect on the liquidity of some businesses in several countries in Asia Pacific.

Nearly half of the respondents in Australia said that the risk of payment delay and default from B2B buyers has increased over the past six months. One in five respondents rated it as “significant”.

62.0% of the businesses surveyed in China (compared to 46.3% in Asia Pacific) reported that domestic B2B customers have slowed invoice payment due to liquidity problems over the past year.

92.1% of respondents in Hong Kong (compared to 90.2% of respondents in Asia Pacific) reported having experienced invoice late payment from their B2B customers over the past year.

38.8% of respondents in India (29.6% in Asia Pacific) said domestic B2B customers pay invoices late intentionally, to use trade credit as a way of alternatively financing their business operations.

30% of survey respondents in Indonesia reported that payment on domestic B2B invoices is received late due to the formal insolvency of the buyer (respondents in Asia Pacific: 21.4%).

Most of the survey respondents in Japan (32.5%, notably above the 23% in Asia Pacific) consider cost containment to be the biggest challenge to business profitability this year.

21.5% respondents in Singapore versus 17.4% in Asia Pacific consider a likely drop in demand for their products and services as the biggest challenge to business profitability in 2015.

32.5% of respondents in Taiwan compared to 25.8% in Asia Pacific said that domestic B2B customers pay invoices late most often due to disputes over the quality of goods delivered or services provided.

Global trade growth has slowed significantly in recent years. For 2015, Atradius predicts just 1% international trade growth. This implies a difficult environment for exporters.

Russia remains an important market in the global economy. The ten principles of the report are meant to help businesses mitigate risks when exporting to Russia.

Due to Brazil’s economic slump and problems along the whole domestic automotive value chain we expect both payment delays and defaults to continue to worsen markedly in the coming months.

After subsequent years of production decreases French subcontractors and suppliers have benefited from the rebound of the French and the European automotive sector.

Like other Spanish industries, the automotive sector was hard hit by the economic crisis, as lower domestic consumption and difficulty accessing financing led to a slump in the car market.

Thanks to the strong recovery seen since H2 of 2014 many of Italy’s car suppliers have registered increasing profit margins and an improvement of their financial strength.

In Slovakia, payment behaviour is generally good with a low number of non-payment notificiations, and this is expected to remain unchanged in the coming months.

Thailand´s automotive sectors is characterised by high entry barriers as the players in the market are large multinationals with strong financials and good know-how.

Economic growth in the resource-rich Brazil continues to remain under pressure due to a combination of a credit crunch, rising interest rates and weakening demand.

One in three businesses surveyed in Brazil, Canada, Mexico and the United States reported that around one-fifth of the value of their B2B receivables is more than 90 days overdue.

Inflation is expected to remain high in 2015, at around 7%, while the current account deficit is expected to remain at the same level as in 2014 (5.7% of GDP).

Growth is expected to accelerate further in 2015 and 2016, by 2.8% and 3.5% respectively, driven by continued robust domestic demand and increasing exports to the Eurozone.

The Polish economy is expected to benefit from low energy prices and the rebound in the Eurozone, with GDP expected to grow 3.5% in 2015, based on robust domestic demand and increasing exports.

The impact of the Chinese stock market crunch of this summer and the renminbi devaluation should not be overestimated. The main long-term risk is an accelerating economic slowdown.

Land acquisition issues in setting up greenfield projects, delays in environmental clearances, logistics support and external financing remain major issues

Structural overcapacity in the industry had a negative effect on businesses´ profit margins in 2014, and this negative trend is expected to continue in 2015.

In 2015, Australian business insolvencies are expected to increase slightly by 2% as economic growth slows down and the mining industry faces mounting troubles.

The sector benefits from higher machinery investments as the Japanese economic recovery is on track (GDP is expected to grow 1.0% in 2015 and 1.5% in 2016 after a modest contraction in 2014).