Ön egy Atradius weboldalra lépett be. Azzal, hogy a weboldalon található valamely funkcióra kattint - az oldal megnyitásakor létrejövő, első cookie-t is beleértve - elfogadja a cookie-k használatából eredő információk tárolására vonatkozó gyakorlatunkat. A sütik használatáról és letiltásáról további információkat talál a Cookie információk oldalon.

Tekintse át az Atradius Collections Nemzetközi követelésbehajtási kézikönyvében, Globális behajtási hírlevél és Iparági trendjelentőjében szereplő globális kereskedelmi követeléskezelési adatokat.

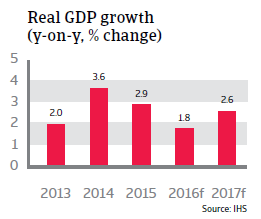

Hozzáférést kaphat az ország 14 fontos ágazatában a hitelkockázati helyzetről és üzleti eredményekről. Az előrejelzés az Atradius kockázatelbírálóinak értékelésén alapszik.

Problems remain in the building sectors of most of the countries covered in this issue of the Market Monitor. Consequently, the outlook for the construction industry in 2015 remains muted.

Problems remain in the building sectors of most of the countries covered in this issue of the Market Monitor. Consequently, the outlook for the construction industry in 2015 remains muted.

Problems remain in the building sectors of most of the countries covered in this issue of the Market Monitor. Consequently, the outlook for the construction industry in 2015 remains muted.

In 2015 we expect the construction sector in Germany to perform well and construction insolvencies to decrease by 3%, less than the 5% decrease forecast for business insolvencies in Germany overall.

A 9 % increase is forecast for the US construction sector in 2015; the vast majority of construction and design firm executives believe the market is stable or growing.

While French business insolvencies are forecast to level off in 2015, it is expected that construction business failures will further increase due to the low economic growth forecast for France.

A sharp Chinese economic slowdown will affect countries through their exports and commodity prices. Especially countries in Asia and Africa are vulnerable.

Vietnam is extremely export-driven, specialising in textiles and footwear. The economy is shifting towards higher value added sectors such as electronics.

After 3.1% growth in 2014, Singapore’s economic growth is expected to accelerate to 3.4% in 2015, driven by investment; among other things, in its infrastructure.

Since 2012, economic growth has been high, driven by private consumption which accounts for about 70% of the economy. Growth has also been sustained by rising demand for exports.

Malaysia’s business environment is considered to be far more favourable than that of its regional neighbours, apart from Singapore, and the financial sector is strong.

As in 2013 and 2014, fierce competition means that the Dutch construction sector is still affected by price wars, leading to on-going pressure on margins.

The swift implementation of reforms would further strengthen Mexico ́s already solid external economic situation by boosting FDI and reducing dependency on volatile portfolio capital inflows.

India’s rebound is expected to be driven by the resumption of stalled infrastructure projects, high investment, urbanisation, the improvement of the business environment and structural reforms.