Ön egy Atradius weboldalra lépett be. Azzal, hogy a weboldalon található valamely funkcióra kattint - az oldal megnyitásakor létrejövő, első cookie-t is beleértve - elfogadja a cookie-k használatából eredő információk tárolására vonatkozó gyakorlatunkat. A sütik használatáról és letiltásáról további információkat talál a Cookie információk oldalon.

Tekintse át az Atradius Collections Nemzetközi követelésbehajtási kézikönyvében, Globális behajtási hírlevél és Iparági trendjelentőjében szereplő globális kereskedelmi követeléskezelési adatokat.

Hozzáférést kaphat az ország 14 fontos ágazatában a hitelkockázati helyzetről és üzleti eredményekről. Az előrejelzés az Atradius kockázatelbírálóinak értékelésén alapszik.

While in general insolvencies are not expected to rise sharply, an increase in business failures in Puerto Rico and the Houston area cannot be ruled out.

Export orientation and diversification are key factors for business success in a business environment characterised by overcapacity and volatile prices.

Due to a high non-performing assets level banks remain reluctant to provide loans, and external financing at competitive conditions remains a challenge.

Payment experience has been good over the past two years, and steel and metals insolvencies decreased in 2016, with a stable outlook for 2017 and 2018.

Banks have generally tightened their lending policies for steel businesses due to the fierce competitive environment and still subdued domestic demand.

Revenues of the engineering services industry have rebounded since 2015 as greater liquidity in financial markets helped to boost construction spending.

Profit margins have increased over the last 12 months due to the benign business environment, however, a slight decline cannot be ruled out in the future.

Due to deteriorated results and margins, as well as increased payment delays and insolvencies our underwriting stance remains restrictive for the sector.

The proportion of domestic and foreign past due B2B invoices in Hong Kong (domestic: 50.0%; foreign: 50.3%) is higher than that recorded at regional level.

The total value of B2B sales on credit in Japan increased this year to 53.7%. Of the Asia Pacific countries surveyed, Japan was the most credit-friendly.

Private consumption is driven by wage growth while export growth is driven by Eurozone demand and the country´s improved international competitiveness.

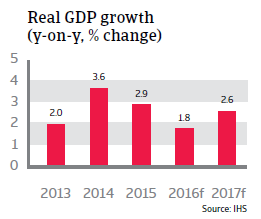

Hungary´s economic growth is expected to rebound in 2017 and 2018 after a slowdown in 2016, but the high level of external debt remains a major weakness.

GDP is expected to grow 4.2% in 2017 and 3.7% in 2018, driven strong private consumption and rising investments including structural funds from the EU.

Despite the current rebound the long-term prospect for higher growth rates is subdued due to structural weaknesses and the negative impact of sanctions.

GDP growth is robust, but risks in the banking and corporate sectors have increased while high dependence on capital inflow remains a major vulnerability.

As more and more carmakers rush to enter into the electric and hybrid car segment, annual capacity in China is about to exceed 7 million units by 2020.

Automotive suppliers´ margins remain structurally under pressure, as the powerful car manufacturers demand greater productivity, coupled with lower prices.

The level of insolvencies in the automotive sector is low compared to other Italian industries, and business failures are expected not to increase in 2017.

A large number of small supplier businesses could face higher business and credit risks in the future as margins have declined and challenges increase.

The Spanish automotive industry continues to benefit from the on-going economic rebound of the domestic economy as well as from increasing car exports.

Robust sales have kept profit margins of car producers and suppliers stable, and these are expected to maintain their current level in the coming months.

Most businesses in the automotive sector should be financially resilient enough to cope with some minor volatility in demand or exchange rate fluctuations.

Atradius forecasts insolvencies across advanced markets to fall by 3.0% this year and 2.0% next year, particularly led by an increasingly robust recovery in the eurozone.