Ön egy Atradius weboldalra lépett be. Azzal, hogy a weboldalon található valamely funkcióra kattint - az oldal megnyitásakor létrejövő, első cookie-t is beleértve - elfogadja a cookie-k használatából eredő információk tárolására vonatkozó gyakorlatunkat. A sütik használatáról és letiltásáról további információkat talál a Cookie információk oldalon.

Tekintse át az Atradius Collections Nemzetközi követelésbehajtási kézikönyvében, Globális behajtási hírlevél és Iparági trendjelentőjében szereplő globális kereskedelmi követeléskezelési adatokat.

Hozzáférést kaphat az ország 14 fontos ágazatában a hitelkockázati helyzetről és üzleti eredményekről. Az előrejelzés az Atradius kockázatelbírálóinak értékelésén alapszik.

Due to limited organic growth opportunities and the on-going economic uncertainty, market players strive to expand through acquisitions and specialisation.

Despite continued sales growth, most German ICT businesses operate on very tight margins due to fierce competition and price erosion in most subsectors.

On average, payments in the ICT sector take between 30 and 90 days. Business culture promotes prompt payment, and therefore the number of delays is low.

After an increase of almost five percentage points in 2016, the percentage of overdue B2B invoices in Eastern Europe decreased again this year (41.5%).

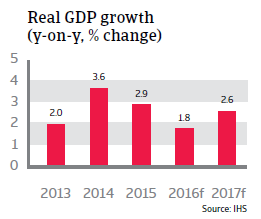

The percentage of overdue B2B invoices in Hungary decreased in 2017. At 29.7%, the payment default rate in the country is far under the regional average.

High uncertainty surrounding NAFTA renegotiations and other US policy directions in international trade, and specifically targeting Mexico, could adversely affect sentiment and investment.

In 2017 the number of Belgian business insolvencies will still be much higher than the levels seen before the start of the global credit crisis in 2008.

Private consumption remains a key driver of growth in 2017, sustained by higher household purchasing power and further decreasing unemployment figures.

Italy´s GDP growth is expected to remain subdued in 2017 as international competitiveness remains an issue and the banking sector is still under pressure.

Wzrost polskiego PKB zwolnił od 2015 r. w związku ze spadkiem poziomu inwestycji. Przewiduje się, że w 2017 r. PKB wzrośnie do poziomu 3,3% z 2,8% w 2016 r.

The use of credit terms for B2B sales by respondents in Western Europe decreased slightly compared to 2016, stressing the challenging business environment.

The percentages of B2B sales on credit terms in Denmark (56.4%) are, as in previous years, significantly higher than in Western Europe overall (38.8%).

In 2017, 29.3% of B2B sales in France were made on credit, far less than the regional average of 38.9%. This is similar to what was observed last year.

Compared to one year ago (31.5%), Greece has seen an increase of almost seven percentage points in the percentage of overdue B2B invoices in 2017 (38.6%).

After Denmark (56.4%) and Greece (52.1%), Ireland has the highest average of sales made on credit terms (48.2%) in the Western European countries surveyed.

After a slight decrease in sales on credit terms in 2016 (44.3%), the total value of B2B sales on credit in Great Britain increased again this year (45.7%).

Compared to the 2016 survey results there has been a reduction in the percentage of both domestic and foreign B2B sales made on credit in the Netherlands.

Compared to 2016, respondents in Spain sold less on credit terms, underlining the downward trend in sales on credit terms observed in previous surveys.

Payment behaviour of many Turkish businesses has deteriorated since 2015, and key sectors continue to face problems in 2017 due to increased uncertainty.

Competition is high in all segments and price pressure offsets sales volume growth, meaning that the already low profit margins will remain under pressure.